Part I of Girlfriend to Girlfriend Money Chat looks at some of the reasons women generally refrain from talking about personal finances with those they’re close with. Then, I share some of the internal struggles I’ve been experiencing, my vision for my girlfriends (and other women around the globe) as related to their financial confidence and sense of empowerment, and a plan of actions so that my behaviors align better with what matter to me.

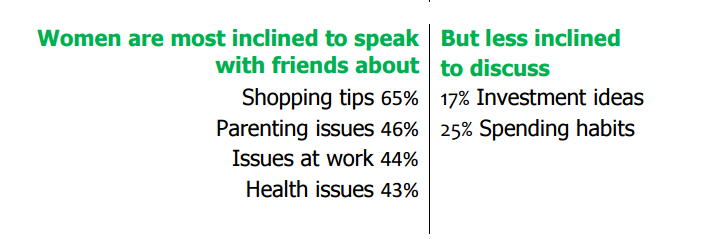

In the same Money Fit Women Study I referenced to in a previous post, the survey also revealed that despite a substantial percentage of women having expressed the desire to become more engaged with their finances, many felt uncomfortable discussing money topics with their friends. Let’s take a look at the statics below:

After reading the survey results, the psychologist in me immediately got to work and started examining the dynamics within my circle of friends.

My Circle of Friends

It’s true that my friends and I rarely discuss our financial situations with each other. I’ve never thought about it this way prior to having read the survey results.

So what did my girlfriends and I typically chat about? Discussion topics usually varied from tips on styling our hair, shopping for a pair of over-the-knee boots, which dentist to go to, who to hire to remodel our kitchen, which tailor to use, how to shop for our significant others, what to wear for a first date, how to cook quinoa, which Netflix show to watch next, how to create a pivot table on Excel, what to wear with a pencil skirt, which bakery offers the best scones, and the list can go on and on. However, our conversations rarely centered around discussing personal finance topics. As most of my girlfriends are currently between the ages of 25 and 40, many of our recent discussion topics revolved around parenting, in-laws, the workplace, health and nutrition, wedding planning, baby showers, personal styles, romantic relationships, career changes, entertainments and leisure travels. We are like a team of experts on those aforementioned topics. Everyone always had something to share and we could all relate one way or another.

Were money concerns just something that didn’t come up? A 2013 Wells Fargo Financial Health Study reported that money is the biggest stress in life for 39% of Americans (survey sampled 1,004 adults, ages 25-75). In the same survey, a third of Americans said they lose sleep worrying about money and 49% expressed regrets about saving and spending in the past five years.

So why don’t we discuss our finances? During all those get-together times, I thought my friends and I didn’t hold back…or at least I thought so until I read about people’s relationships with money and started examining my own life and those around me.

It turns out that in general nearly half of Americans (44%) said the most challenging topic to discuss with others is personal finances, whereas death (38%), politics (35%), religion (32%), and personal health (20%) ranked as less difficult (source).

Sure, my girlfriends and I loved texting each other when we found double coupons or alerting each other when an item had a price reduction. Yet, we had no idea how much each of us were spending on clothes, bags and shoes each year. We’ve causally shared how much we spent on the wedding photographer, our hospital bills for labor, the amount we spend on daycare, or the price we paid for a single bag. But these numbers were readily available. Money was certainly involved, but there was nothing too personal about this kind of sharing. We recommended which CPA to use filing tax returns, but we didn’t share how much tax we owed or how much money we were getting back. We shared how much we spent going on a helicopter ride while visiting Hawaii, but we left out that we also purchased a timeshare during the trip. We shared that we own a house and a rental, but left out that we only paid 20% down payment on each and that we were still struggling to pay off over $50,000 student loans. We bragged that we didn’t have debt, and left out that we were living paycheck to paycheck. We shared that we had health insurance, but left out that we were paying over $700 to insure a family of 4 each month.

Yes, we talked about money, but we always felt hesitant and/or reluctant to fully expose our financial situations. At the same time, very few of us felt comfortable asking another person where the money was coming from or questioned motivations and reasoning behind her financial decisions. Those of us who were listening might have shared a “look” with each other by raising our eyebrows, and the topic of discussion quickly got changed.

My Internal Struggles

I, too, feel uncomfortable discussing my financial situation with my closest girlfriends. Just thinking about it gives me goosebumps. This has nothing to do with how financially savvy I am.